This document was ed by and they confirmed that they have the permission to share it. If you are author or own the copyright of this book, please report to us by using this report form. Report 2z6p3t

Overview 5o1f4z

& View Audit & Settlement Of Audit Objections (mr.ifftikhar Ahmed).ppt as PDF for free.

More details 6z3438

- Words: 2,151

- Pages: 37

1

AUDIT AND SETTLEMENT OF AUDIT OBSERVATIONS IFTIKHAR AHMAD DIRECTOR GENERAL AUDIT WORKS (PROVINCIAL) LAHORE 2

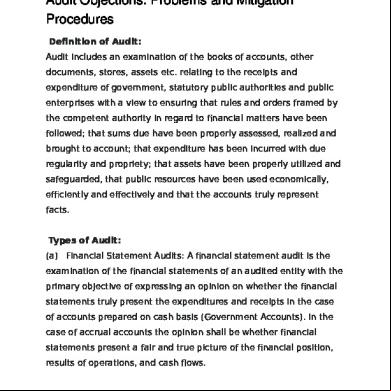

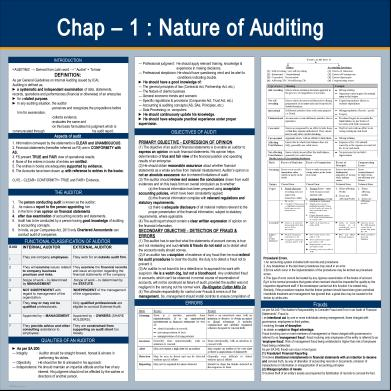

AUDITING 1. Definition Audit is an independent examination of the financial statements of an organization / enterprise by an appointed auditor in pursuance of his appointment and in compliance with the relevant statutory obligations. In general, audit is a mechanism within the process of ability where the performance of the resources of an organization is checked on behalf of interested parties. 3

2.

Origin of Audit

3.

Objectives of Auditing i.

Detection of errors and omissions.

ii. Detection of loss caused to the organization by reason of fraud. iii. Expression of independent opinion on ing. iv. Moral check.

4

4.

Scope of Audit

The scope of auditing depends on many things like: i. Constitutional Provisions. ii.Statutory obligations. iii.Regulations of relevant entity. iv. of reference defined in the letter of engagement.

5

5. Types of Audit i.

Internal Audit

(Audit conducted by the Internal Auditors)

ii. External Audit

(Audit conducted by the External Auditors)

iii. Performance Audit

(About the performance of the organization)

iv. Certification Audit

(Certification of s).

v. System based Audit

(To review the working of internal control)

vi. Policy Audit

(Economic, financial and social costs of govt. policies)

vii. Management Audit

(Audit the decisions of management)

viii.Programme Audit

(Audit of Projects)

6

6. List of Auditable Documents i.

Cash book

ii.

Stock

iii.

Pay bills / Acquaintance Rolls

iv.

Contingent

v.

Service Books

vi.

Log Books

vii.

Contingent Bills

viii.

Auction File

ix.

Monthly Expenditure Statement 7

7. Qualities of an Auditor i.

Professional Knowledge

ii.

Integrity

iii.

Intelligence and tact

iv.

Impartiality

v.

Courtesy

vi.

Confidentiality

8

7. Qualities of an Auditor (conti….) vii.

Vigilance

viii.

Positive attitude

ix.

Diligence

x.

Communication Skill

9

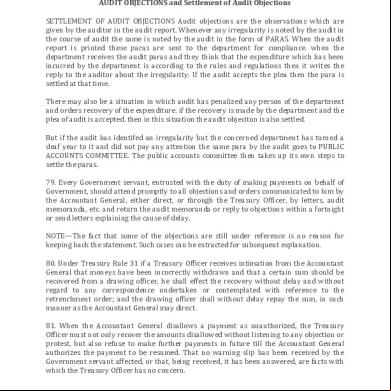

8. Audit Procedure (How Audit Paras are Prepared?) i. Audit & Inspection Report (AIR) a result of an audit activity. ii. Ordinary Paras and Advance Paras iii. Proposed Draft Paras iv. Draft Paras and Audit Report

10

9. Nature of Audit Observations i. Misappropriation (embezzlement) ii. Recoverable iii. Overpayments iv. Violation of Rules v. Non-Production of Records vi. Others 11

10. Settlement of Audit Paras i.

DAC

(Departmental s Committee)

ii. SDAC

(Special Departmental A/cs Committee)

iii. PAC

(Public s Committee)

12

i.

DAC

(Departmental s Committee)

It is constituted by the orders of the President, in case of Federation and by the Governor, in case of Province.

Brief History of DAC: The first DAC in Punjab was constituted in Nov.1959 by the orders of the Governor West Pakistan. The same orders were reiterated in Dec.1982 for strict compliance.

Purpose of DAC: Prompt action by the department for attendance / settlement of irregularities notices in audit and reported in Inspection Reports issued by the Audit Department.

13

of DAC in Punjab i. Secretary to the Govt. of the concerned department

(Chairman)

ii. A representative of Finance Department

(Member)

iii. A representative of the Audit Department concerned

(Member)

iv. If the Secretary is unable to preside over the meeting, the Additional Secretary / Deputy Secretary of the Department should chair the meeting. v. The participation of the representative of istrative Secretary not below the rank of Deputy Secretary is essential. vi. The notice and working papers for the meeting should be sent to Audit Office concerned at least a week before the date of meeting. 14

Meeting of the DAC Periodic meeting of each of each committee will be convened by the chairman at regular intervals in connection with Finance Department and Audit Department concerned.

Function of DAC i. The Committee will examine the irregularities pointed out by Audit through their Inspection Reports or otherwise and recommend action to be taken in respect of irregularities. ii. It will be the duty of Secretary of the istrative Department concerned to obtain Govt. orders ordinarily within one month of the date of recommendation made by the Committee.

15

SDAC:

(Special Departmental s Committee)

Purpose: Prompt action by the department for attendance / settlement of Advance Paras / Proposed Draft Paras.

: i.

Secretary or Additional Secretary of the Department concerned. (Chairman)

ii. A representative of the Finance Department of appropriate level. (Member) iii.

A representative of the Audit Department of appropriate level. (Member)

16

Working Papers: i. Working paper of at least 25 Audit Papers. ii. Working paper duly ed by relevant documents will be submitted to the Director General Audit concerned. iii. Working paper should contain a certificate that no Draft Paras has been included therein. iv. Settlement of paras takes place if the department shows compliance.

17

PAC:

(Public s Committee)

Constitutional Role of PAC i. The main function of the PAC Committee is to see that the money granted by the legislature has been spent by the executive within the scope of the demand. The Committee has, therefore, to satisfy itself by: a.

The money recorded as spend against the grant was actually spent and was not larger than the amount granted. b. The money has not been spent for a purpose not approved by the legislature. c.

There are no other irregularities in the spending of the public money by the executive. 18

ii. Where the Auditor General Audit s of receipts and of stores and stocks, the Committee also considers the audit report there on in much the same details as in the case of expenditure. The commercial s of the Public Commercial and Industrial Organizations are also considered in the same way. iii.The committee has the power to examine the representatives of the departments concerned and to summon the officers move directly responsible, where necessary. 19

iv.The Committee is entitled to offer criticism and recommendations upon any matter discussed in the appropriation s or in the audit report thereon; v. The report and recommendations of the Committee are discussed in the National Assembly / Provincial Assembly. 20

Limitations of Audit i. Advisory role. ii. No authority to penalize the auditee. iii. Orthodox methods of auditing. iv. Incompetent audit staff. v. Late consideration of Audit Report in PAC vi. Element of corruption / dishonesty by the auditors. vii. Non-availability of facilities incentives to the Auditors. viii. Non-availability of safety protection against threats from auditees especially Police Deptt. ix. Efficiency of the Auditors depends on the number of paras not on quality of paras.

21

Appropriation s The Appropriation s and the Report thereon consist of the Appropriation proper and the Audit Report thereon. The Audit Report giver the general view of the results of audit and draws attention to important matters, if any, outstanding from the previous Reports. The Appropriation s proper consist of: -

22

a). a grand summary giving a general view of the total expenditure under each Grant / Appropriation compared with the total Grant / Appropriation sanctioned there under. b). audited s of all the expenditure of the year, whether “Authorized” or “Charged” in the form of a separate appropriation for each Grant / Appropriation, with any important observations which it is considered necessary to make as a result of audit investigation, and c).

the financial irregularities, including cases relating to any previous year that become ripe for inclusion since the last report was written, which are of sufficient consequence to justify inclusion. 23

Finance s The Finance s and Report thereon deal with the s of the Province as a whole including transactions relating to debt, deposits, sinking funds, advances suspense s and remittance business and general financial matters that do not strictly fall within the functions of the Public s Committee as laid down in rule 15 of the rules of Procedure of the Provincial Assembly of the Punjab which have been reproduced in Part II of Appendix A. This document though laid before the Provincial Assembly is not referred to the Public s Committee. After it is laid before the Provincial Assembly, the Finance Department should examine it and take action wherever it is called for and report the action taken to ant General, Punjab. 24

Statutory Obligations of Audit The private ed companies are legally bound to get their s audited from independent auditors. The government s are audited by the Auditor General of Pakistan. The Auditor General of Pakistan is appointed under Article 68 of the Constitution of Pakistan. He is responsible for keeping the s of federation and each province other than departmentalize offices like Defence, Railway, Postal Services, Pakistan Telecommunication, Pakistan Mint, National Savings, Foreign Affairs, Food Wing, Forest, Pak PWD. 25

Duties / Functions / Powers of the Auditor General of Pakistan 1. It shall be the duty of Auditor General to: i.

Audit all the expenditure and ascertain that the money is legally available and expenditure conform to the authority;

ii.

Audit all transactions of public s of the federation and each province;

iii.

Audit all trading, manufacturing and profit & loss and balance sheets; and

iv.

Audit the s of any body or authority of federation and provinces. 26

2.

Auditor General may audit and report on:i. The receipts of any department. ii. The s of stores & stocks. The Auditor General has the power to inspect any treasury or office (Para-15 of A&A Order- 1973).

3. 4.

The Auditor General has the power to call for any information from any office under this jurisdiction. Auditor General can frame Rules and to give directions in all matters to audit of expenditure, transactions and s. These directions, methods and extent of audit are contained in the codes and manuals.

27

Settlement of Audit paras in District Government Financial System

Under Local Government Ordinance 2001, Article 115 deals with audit of the District Govt. 1. The Director Local Fund Audit shall conduct regular annual audit of the Local Funds and the Director-General Audit of the Province shall undertake audit of the District, Tehsil and Town Provincial s during a financial year. 2. Upon request of a Nazim, the Provincial Director, Local Fund Audit, shall cause to be conducted an audit of the respective Local Fund. 3. Upon request of a Zila Nazim, Tehsil Nazim or Town Nazim the Director-General Audit of the Province shall cause the audit of District Provincial , Tehsil Provincial or, the case may be, Town Provincial and shall forward his report to the concerned Nazim and Council. 4. The report of the Local Fund Audit shall be placed before the concerned Nazims and the s Committee of the respective Councils for necessary action.

28

5.

The Provincial Director-General Audit shall conduct the external audit of each District Government, Tehsil Municipal istration, Town Municipal istration and Union istration, in the prescribed manner, once in a financial year and place the report before the Public s Committee of the Provincial Assembly and the s Committee of the respective Council. 6. The Local Government Commission of a Province may cause for a special audit of the s of a local government as provided for in section 132. 7. The Provincial Director-General Audit or an officer appointed by him, or Director, Local Fund Audit for conducting an audit of a local government and shall have access to all the books and documents pertaining to the s, and may also examine any member, servant or premises of the local government concerned. 29

How to avoid Audit Objections & Financial Irregularities

i. be well versed with financial rules. ii. Expenditure be incurred within the valid sanction. iii. Availability of budget be ensured. iv. Documentation be proper. v. Proper maintenance of s record be ensured. vi. Internal audit be started in the organization.

30

vii. Up-dation of budgetary figures with the Headquarter be ensured. viii. Purchase procedure laid down by the department be followed. ix. Audit observations once taken by the audit in a year should be repeated next year. x. Reply of audit observations be given within stipulated period. xi. Follow the advisory remarks of the audit about the organization. xii. Expenditure be made in the public interest.

31

Advantages of Auditing 1. Detection and prevention of errors and frauds become easier 2. Audited ing information, greater reliability and authenticity 3. Acceptability by the authorities 4. Speedy processing of loans 5. Settlement of disputes in partnership 32

Advantages of Auditing (cont….) 6. Facilitates calculations of net worth and good will of business 7. Professional advice available 8. Settlement of issuance claims 9. Useful to compare the financial performance 10.Keeps s department vigilant 11.Identifies the weak areas

33

Audit Exercise Mr. ABC is working as DDO in an organization. What steps he should exercise while making the budgetary spending under each head in his office?

34

Solution 1. Provision of funds 2. Sanctions of expenditures 3. Claims on proper format 4. Period of sanction 5. Rules of payment

35

Solution (Conti…..) 6. Payment mode (cheque or cash) 7. Classification of expenditure 8. Payment on prescribed rates 9. ing of payments 10.Reconciliation with s office

36

Thank You 37

AUDIT AND SETTLEMENT OF AUDIT OBSERVATIONS IFTIKHAR AHMAD DIRECTOR GENERAL AUDIT WORKS (PROVINCIAL) LAHORE 2

AUDITING 1. Definition Audit is an independent examination of the financial statements of an organization / enterprise by an appointed auditor in pursuance of his appointment and in compliance with the relevant statutory obligations. In general, audit is a mechanism within the process of ability where the performance of the resources of an organization is checked on behalf of interested parties. 3

2.

Origin of Audit

3.

Objectives of Auditing i.

Detection of errors and omissions.

ii. Detection of loss caused to the organization by reason of fraud. iii. Expression of independent opinion on ing. iv. Moral check.

4

4.

Scope of Audit

The scope of auditing depends on many things like: i. Constitutional Provisions. ii.Statutory obligations. iii.Regulations of relevant entity. iv. of reference defined in the letter of engagement.

5

5. Types of Audit i.

Internal Audit

(Audit conducted by the Internal Auditors)

ii. External Audit

(Audit conducted by the External Auditors)

iii. Performance Audit

(About the performance of the organization)

iv. Certification Audit

(Certification of s).

v. System based Audit

(To review the working of internal control)

vi. Policy Audit

(Economic, financial and social costs of govt. policies)

vii. Management Audit

(Audit the decisions of management)

viii.Programme Audit

(Audit of Projects)

6

6. List of Auditable Documents i.

Cash book

ii.

Stock

iii.

Pay bills / Acquaintance Rolls

iv.

Contingent

v.

Service Books

vi.

Log Books

vii.

Contingent Bills

viii.

Auction File

ix.

Monthly Expenditure Statement 7

7. Qualities of an Auditor i.

Professional Knowledge

ii.

Integrity

iii.

Intelligence and tact

iv.

Impartiality

v.

Courtesy

vi.

Confidentiality

8

7. Qualities of an Auditor (conti….) vii.

Vigilance

viii.

Positive attitude

ix.

Diligence

x.

Communication Skill

9

8. Audit Procedure (How Audit Paras are Prepared?) i. Audit & Inspection Report (AIR) a result of an audit activity. ii. Ordinary Paras and Advance Paras iii. Proposed Draft Paras iv. Draft Paras and Audit Report

10

9. Nature of Audit Observations i. Misappropriation (embezzlement) ii. Recoverable iii. Overpayments iv. Violation of Rules v. Non-Production of Records vi. Others 11

10. Settlement of Audit Paras i.

DAC

(Departmental s Committee)

ii. SDAC

(Special Departmental A/cs Committee)

iii. PAC

(Public s Committee)

12

i.

DAC

(Departmental s Committee)

It is constituted by the orders of the President, in case of Federation and by the Governor, in case of Province.

Brief History of DAC: The first DAC in Punjab was constituted in Nov.1959 by the orders of the Governor West Pakistan. The same orders were reiterated in Dec.1982 for strict compliance.

Purpose of DAC: Prompt action by the department for attendance / settlement of irregularities notices in audit and reported in Inspection Reports issued by the Audit Department.

13

of DAC in Punjab i. Secretary to the Govt. of the concerned department

(Chairman)

ii. A representative of Finance Department

(Member)

iii. A representative of the Audit Department concerned

(Member)

iv. If the Secretary is unable to preside over the meeting, the Additional Secretary / Deputy Secretary of the Department should chair the meeting. v. The participation of the representative of istrative Secretary not below the rank of Deputy Secretary is essential. vi. The notice and working papers for the meeting should be sent to Audit Office concerned at least a week before the date of meeting. 14

Meeting of the DAC Periodic meeting of each of each committee will be convened by the chairman at regular intervals in connection with Finance Department and Audit Department concerned.

Function of DAC i. The Committee will examine the irregularities pointed out by Audit through their Inspection Reports or otherwise and recommend action to be taken in respect of irregularities. ii. It will be the duty of Secretary of the istrative Department concerned to obtain Govt. orders ordinarily within one month of the date of recommendation made by the Committee.

15

SDAC:

(Special Departmental s Committee)

Purpose: Prompt action by the department for attendance / settlement of Advance Paras / Proposed Draft Paras.

: i.

Secretary or Additional Secretary of the Department concerned. (Chairman)

ii. A representative of the Finance Department of appropriate level. (Member) iii.

A representative of the Audit Department of appropriate level. (Member)

16

Working Papers: i. Working paper of at least 25 Audit Papers. ii. Working paper duly ed by relevant documents will be submitted to the Director General Audit concerned. iii. Working paper should contain a certificate that no Draft Paras has been included therein. iv. Settlement of paras takes place if the department shows compliance.

17

PAC:

(Public s Committee)

Constitutional Role of PAC i. The main function of the PAC Committee is to see that the money granted by the legislature has been spent by the executive within the scope of the demand. The Committee has, therefore, to satisfy itself by: a.

The money recorded as spend against the grant was actually spent and was not larger than the amount granted. b. The money has not been spent for a purpose not approved by the legislature. c.

There are no other irregularities in the spending of the public money by the executive. 18

ii. Where the Auditor General Audit s of receipts and of stores and stocks, the Committee also considers the audit report there on in much the same details as in the case of expenditure. The commercial s of the Public Commercial and Industrial Organizations are also considered in the same way. iii.The committee has the power to examine the representatives of the departments concerned and to summon the officers move directly responsible, where necessary. 19

iv.The Committee is entitled to offer criticism and recommendations upon any matter discussed in the appropriation s or in the audit report thereon; v. The report and recommendations of the Committee are discussed in the National Assembly / Provincial Assembly. 20

Limitations of Audit i. Advisory role. ii. No authority to penalize the auditee. iii. Orthodox methods of auditing. iv. Incompetent audit staff. v. Late consideration of Audit Report in PAC vi. Element of corruption / dishonesty by the auditors. vii. Non-availability of facilities incentives to the Auditors. viii. Non-availability of safety protection against threats from auditees especially Police Deptt. ix. Efficiency of the Auditors depends on the number of paras not on quality of paras.

21

Appropriation s The Appropriation s and the Report thereon consist of the Appropriation proper and the Audit Report thereon. The Audit Report giver the general view of the results of audit and draws attention to important matters, if any, outstanding from the previous Reports. The Appropriation s proper consist of: -

22

a). a grand summary giving a general view of the total expenditure under each Grant / Appropriation compared with the total Grant / Appropriation sanctioned there under. b). audited s of all the expenditure of the year, whether “Authorized” or “Charged” in the form of a separate appropriation for each Grant / Appropriation, with any important observations which it is considered necessary to make as a result of audit investigation, and c).

the financial irregularities, including cases relating to any previous year that become ripe for inclusion since the last report was written, which are of sufficient consequence to justify inclusion. 23

Finance s The Finance s and Report thereon deal with the s of the Province as a whole including transactions relating to debt, deposits, sinking funds, advances suspense s and remittance business and general financial matters that do not strictly fall within the functions of the Public s Committee as laid down in rule 15 of the rules of Procedure of the Provincial Assembly of the Punjab which have been reproduced in Part II of Appendix A. This document though laid before the Provincial Assembly is not referred to the Public s Committee. After it is laid before the Provincial Assembly, the Finance Department should examine it and take action wherever it is called for and report the action taken to ant General, Punjab. 24

Statutory Obligations of Audit The private ed companies are legally bound to get their s audited from independent auditors. The government s are audited by the Auditor General of Pakistan. The Auditor General of Pakistan is appointed under Article 68 of the Constitution of Pakistan. He is responsible for keeping the s of federation and each province other than departmentalize offices like Defence, Railway, Postal Services, Pakistan Telecommunication, Pakistan Mint, National Savings, Foreign Affairs, Food Wing, Forest, Pak PWD. 25

Duties / Functions / Powers of the Auditor General of Pakistan 1. It shall be the duty of Auditor General to: i.

Audit all the expenditure and ascertain that the money is legally available and expenditure conform to the authority;

ii.

Audit all transactions of public s of the federation and each province;

iii.

Audit all trading, manufacturing and profit & loss and balance sheets; and

iv.

Audit the s of any body or authority of federation and provinces. 26

2.

Auditor General may audit and report on:i. The receipts of any department. ii. The s of stores & stocks. The Auditor General has the power to inspect any treasury or office (Para-15 of A&A Order- 1973).

3. 4.

The Auditor General has the power to call for any information from any office under this jurisdiction. Auditor General can frame Rules and to give directions in all matters to audit of expenditure, transactions and s. These directions, methods and extent of audit are contained in the codes and manuals.

27

Settlement of Audit paras in District Government Financial System

Under Local Government Ordinance 2001, Article 115 deals with audit of the District Govt. 1. The Director Local Fund Audit shall conduct regular annual audit of the Local Funds and the Director-General Audit of the Province shall undertake audit of the District, Tehsil and Town Provincial s during a financial year. 2. Upon request of a Nazim, the Provincial Director, Local Fund Audit, shall cause to be conducted an audit of the respective Local Fund. 3. Upon request of a Zila Nazim, Tehsil Nazim or Town Nazim the Director-General Audit of the Province shall cause the audit of District Provincial , Tehsil Provincial or, the case may be, Town Provincial and shall forward his report to the concerned Nazim and Council. 4. The report of the Local Fund Audit shall be placed before the concerned Nazims and the s Committee of the respective Councils for necessary action.

28

5.

The Provincial Director-General Audit shall conduct the external audit of each District Government, Tehsil Municipal istration, Town Municipal istration and Union istration, in the prescribed manner, once in a financial year and place the report before the Public s Committee of the Provincial Assembly and the s Committee of the respective Council. 6. The Local Government Commission of a Province may cause for a special audit of the s of a local government as provided for in section 132. 7. The Provincial Director-General Audit or an officer appointed by him, or Director, Local Fund Audit for conducting an audit of a local government and shall have access to all the books and documents pertaining to the s, and may also examine any member, servant or premises of the local government concerned. 29

How to avoid Audit Objections & Financial Irregularities

i. be well versed with financial rules. ii. Expenditure be incurred within the valid sanction. iii. Availability of budget be ensured. iv. Documentation be proper. v. Proper maintenance of s record be ensured. vi. Internal audit be started in the organization.

30

vii. Up-dation of budgetary figures with the Headquarter be ensured. viii. Purchase procedure laid down by the department be followed. ix. Audit observations once taken by the audit in a year should be repeated next year. x. Reply of audit observations be given within stipulated period. xi. Follow the advisory remarks of the audit about the organization. xii. Expenditure be made in the public interest.

31

Advantages of Auditing 1. Detection and prevention of errors and frauds become easier 2. Audited ing information, greater reliability and authenticity 3. Acceptability by the authorities 4. Speedy processing of loans 5. Settlement of disputes in partnership 32

Advantages of Auditing (cont….) 6. Facilitates calculations of net worth and good will of business 7. Professional advice available 8. Settlement of issuance claims 9. Useful to compare the financial performance 10.Keeps s department vigilant 11.Identifies the weak areas

33

Audit Exercise Mr. ABC is working as DDO in an organization. What steps he should exercise while making the budgetary spending under each head in his office?

34

Solution 1. Provision of funds 2. Sanctions of expenditures 3. Claims on proper format 4. Period of sanction 5. Rules of payment

35

Solution (Conti…..) 6. Payment mode (cheque or cash) 7. Classification of expenditure 8. Payment on prescribed rates 9. ing of payments 10.Reconciliation with s office

36

Thank You 37

Related Documents c2h70

Audit Objection And Settlement Of Audit Objections 2a5m4y

November 2021 0

Audit Objections 323d1w

November 2021 0

July 2020 0

Audit 2ct40

October 2020 0

Audit 2ct40

April 2022 0

Audit 2ct40

December 2020 0More Documents from "Mudassar Nawaz" 69i42

Precis Manual (solution ) R.dhillon 3p6z56

January 2022 0

July 2020 0

Css-pms Islamiat Notes In Urdu (complete) 1f5e4a

October 2019 504

A Training Module For Retail Srore 5fk4c

October 2019 32

Principles Of ing In New ing Model k3526

December 2019 43