Case Solution - Vershire Company 4i1h2l

This document was ed by and they confirmed that they have the permission to share it. If you are author or own the copyright of this book, please report to us by using this report form. Report 2z6p3t

Overview 5o1f4z

& View Case Solution - Vershire Company as PDF for free.

More details 6z3438

- Words: 2,087

- Pages: 6

1

several

shows

divi-

the

to

1

man-

with largest

the Exhibit Reporting

States.

of

company

packaging division-one

United

division.

the

in

Can

Aluminum

cans

Can

diversified

a

was

Aluminum the

for

beverage

the

Company chart

aluminum

including

Vershire

of

divisions, organization

the

ufacturers

major

1996

Company

In

Vershire

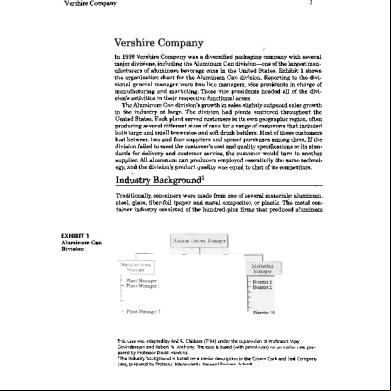

sional general manager were two line managers, vice presidents in charge of manufacturing and marketing. These vice presidents headed all of the division's activities in their respective functional areas.

The Aluminum Can division's growth in salesslightly outpacedsalesgrowth in the industry at large. The division had plants scattered throughout the United States. Each plant served customers in its own geographic region, often producing several different sizes of cans for a range of customers that included

both large and small breweries and soft drink bottlers. Most of these customers had between two and four suppliers and spread purchases among them. If the division failed to meet the customer's cost and quality speciijcations or its stan-

dards for delivery and customer service,the customer would turn to another supplier. All aluminum can producers employed essentially the same technology, and the division's product quality was equal to that of its competitors.

con-

aluminum,

metal

The

materials: plastic.

or

several

of

one composite),

from

made

metal

and

were (paper

fiber-foil

glass,

steel,

containers

Backgroundl

Traditionally,

Industry

tainer industry consisted of the hundred-plus firms that produced aluminum

EXHIBIT 1

AluminumCan

Vijay

Professors

of

supervision

the

(T'94)

Chitkar~

This case was adapted by Anil R.

under

Division

Hawkins.

David

Professor

by

pared

Govindarajanand RobertN. Anthony.The caseis based(with permission)on ~n earliercasepre-

Harvarn

Hamerm~h

Professor

by

prepared

case,

1Theindustry backgroundis basedon a similardescriptionin the Crown Cork and SealCompany R".inA" -:rh~1

2

Company

and tin-plated steel cans. Aluminum cans were used for packaging beverages (beer and soft drinks), while tin-plated steel cans were used primarily for food packaging, paints, and aerosols. In 1970, steel cans ed for 88 percent of metal

pri-

of were

percent

75 containers

over

the

for

had come to dominate

purchased

ed who

cans bottlers

aluminum

but by the 1990s aluminum

drink

soft

1996,

In production.

The

industry.

the can

the metal can production,

cost

64

it for

and

lines

five

ed

was typically

plant

container

materials

a Raw

for line.

scale per

efficient equipment

in

minimum

The

million

$20

ket.

marily small independent franchisees of Coca-Cola and Pepsi Cola, which represented their independent bottlers in negotiating with the container companies. Five beverage container manufacturers ed for 88 percent of the mar-

percent of the production cost. Other costs included labor (15 percent), marketing and general istration (9 percent), transportation (8 percent), depreciation (2 percent), and research and development (2 percent). For beverage processors, the cost of the can usually exceeded the cost of the contents, with the container ing for approximately 40 percent of the to-

tal manufacturing cost.Most beverageprocessorsmaintained two or more suppliers;

and

some

processors

integrated

backward,

manufacturing

cans

themselves.On~ large beveragecompany produced one-third of its own container requirements and ranked ducers in the industry.

as one of the top five beverage container

pro-

efficient,

a more

and

cup even

deep

a become

into had

pushed process

was

metal

of manufacturing

sheet the

flat

a

producing

1996

By

which

in attached.

process was

top

piece

Prior to the early 1970s, cans were produced by rolling a sheet of steel, soldering and cutting it to size, and attaching both the top and the bottom. In 1972 the industry was revolutionized when aluminum producers perfected a two-

over 2,000 cans per minute.

In addition to production efficiency,aluminum had other advantagesover

a

was

reduced

it

and

it pernlitted

aluminum

lithograph;

to

of flavoring;

Additionally;

easier

was

weight.

it lighter

its

because

of

because

packaging costs

attractive

more

steel: It was easier to shape; it reduced the problems

transportation

Vershire

more attractive recycling material, with a ton of scrap aluminum having almost three times the value of a ton of scrap steel. Four global companies supplied alu-

minum to can producers:Alcoa,Alcan, Reynolds,and Kaiser.Two of thesecompanies, Alcoa and Reynolds, also manufactured

Divisions

of Vershire

Company

were structured

aluminum

containers.

to encom

broad product

categories. Divisional general managers were given full control of their busi-

nesseswith two exceptions:the raising of capital and labor relations,which were both centralized at head office. The budget was used as the primary to direct each division's efforts towards common corporate objectives.

tool

In May,eachdivisionalgeneralmanagersubmitteda preliminaryreport to corporate

management

summarizing

the outlook

for sales,

income.

and caDital

3

Company

re-

detailed

not

already

were

was

reports

division

These

each

since

years.

two together

pull

to

subsequent

the

easy

over

fairly

category

usually

each

were

and

in

requirements for the next budget year, and evaluating the trends anticipated

quired to predict market conditions in the current year and to anticipate capital expenditures five years out as part of the strategic planning process. Once the divisional

general

managers

had submitted

these preliminary

re-

to

fore-

budget sales combined

A

forthcoming

were

.

the general

forecasts

these

more

exaInining in and

years division;

each

two

assessment,

market

following

for

the

formal prepared

and

more

a

detail

then

in was

year

velop

ports, the central market researchstaff at corporateheadquartersbeganto de-

cast

Vershire

create a forecast for the entire company. In developing division forecasts, the research staff considered several topics, including general econoInic conditions and their impact on customers, and market share for different products by geographic area. Fundamental assumptions were made as to price, new products, changes in particular s, new

plants, inventory carryovers, forward buying, packaging trends, industry growth trends, weather conditions, and alternative packaging.Each product line, regardlessof size,was reviewed in the samemanner. These foreca~ts were prepared at the head office in order to ensure that basic assumptions were uniform and that overall corporate sales forecasts were

both reasonable and achievable.The completed forecasts were forwarded to their

respective

divisions

for review,

criticism,

and fine-tuning.

The divisional general managers then compiled their own sales forecasts from

the bottom

up, asking

each district

sales manager

to estimate

sales for the

comingbudget year.The district managerscould requesthelp from the head office or the divisional staff but in the end assumed full responsibility for the forecasts they submitted. All district sales forecasts were consolidated at the division level for review by the vice president for marketing, but no changes were made in a district's forecast unless the district manager agreed. Likewise, once the budget had been approved, any changes had to be approved by all those responsible for that budget.

This processwas then repeated at the corporatelevel. When all the responsible parties were satisfied with the sales budget, the figures became fIXed ob-

jectives,with eachdistrict being held responsiblefor its own portion. The entire review

and approval

process

had

four

objectives:

1. To assesseachdivision's competitiveposition and formulate coursesof action to improve

upon

it.

2. To evaluate actions taken to increase market share or to respond to competitors'

activities.

3. To considerundertaking capital expendituresor plant alterations to improve existing

products

or introduce

new products.

4. To developplans to improve cost efficiency,product quality, delivery methods, and service.

~~facturing~~~~~ Mer

final approval at the divisional and corporate levels, the overall sales

budget was translated into a salesbudget for each plant, broken down accord-

4

end use. Onc~ the sales numbers

were estimated,

budgeted

plant

and

the

At volume,

shipped.

each plant

price,

be

to

would according

goods

finished

categorized

the then

which

was

from budget

plants sales

the

to

the

level,

ing

Company

gross profit,

fIXed expenses,and pretax income. Profit was calculated as the sales budget less budgetedvariable costs(including direct material, direct labor, and variable manufacturing overhead-each valued at a standard rate) and the fixed overhead budget. The plant manager was held responsiblefor this budgeted profit number even if actual sales fell below the projected level. Cost standards and cost reduction targets were developed by the plant's industrial engineering department, which also determined budget performance standards for each department, operation, and cost center within the plantincluding such items as budgeted cost reductions, allowances for unfavorable

variancesfrom standards,and fixed costssuch as maintenancelabor. Before plant budgets were submitted, controller staff from the head office visited each plant. These visits were extremely important because they provided an opportunity for plant managers to explain their situation and allowed controllers to familiarize themselves with the reasoning behind the managers' numbers so that they could better explain them when they were presented to corporate management. The controllers also used these visits to provide guidance as to whether the budgeted profits were in line with corporate goals, and

to reinforce the' notion that headquarters was in touch with the plant. Each visit usually lasted about half a day. Most of the time was devotedto

ployees

were

plant

em-

a the

for what)

allocated

(and

also how

was

time

but

themselves

for

see

meetings;

the

could

in

include

controllers

to

so

wished walk-through

agers

reviewing the budget with the plant manager and any supervisors the man-

doing.

On or beforeSeptember1,plant budgetswere submitted to the division head

When

for

was

ap-

asked

for

or

budget

savings. submitted

it

the

additional

budget,

was

approved

the

for

look

either December.

in

budget

who

with

to

asked

satisfied (CEO), consolidated meeting

final

Officer

was

were

managers

Directors

of

Board

The

Executive

manager

plant

general Chief the

at

modifications.

the

divisional

to certain

sent

the

expectations,

office, where they were consolidated and presented to the divisional general managers for review. If the budgets were not quite in line with management's

proval

Vershire

Oncea budget had been approved,it was difficult to change.Any problems that arose between sales and production at a given plant were expected to be solved by people in the field. If a customer called with a rush order that would disrupt production, for example, production could recommend various courses of

action but it was the salesmanager'sresponsibility to get the product to the customer. If the sales manager determined that it was essential to ship the product

right away,that would be done.The customerwas alwaysthe primary concern. Performance

--

Measurement

and

Evaluation

On the secondbusinessday after the closeof eachmonth, every plant faxed certain critical operating varianceswhich were combinedinto a "variance analysis sheet."A compilation of all variance sheetswas distributed the following morning to interested management. Plant managers were not supposed to wait until these monthly statements were prepared to identify unfavorable variances;

Vershire Comoanv

5

rather, they were expectedto be aware of them (and to take correctiveaction)on a daily

basis.

which budgetedtargets had not beenmet.The focuswason net sales,in-

in

areas

Four business days after the close of every month, each plant submitted a report showing budgeted and actual results. Onee these reports were received, corporate management reviewed the variances for those items where figures exceededbudgetary amounts, thus requiring plant managers to explain only the cluding price and mix changes, gross margin, and standard manufacturingcosts. The budgeted and actual information submitted is summarized in Exhibit 2. Supplemental information was provided by ing documents (see Exhibit

3). Both reports were consolidatedfor eachdivision and for the entire company, and distributed

the next day.

The fIXedcostswere examinedto seeif the plants had carried out their various programs,if the programs had met budgetedcosts,and if the results were expectations.

deliv-

and

and

mix, operations

sales plant

price,

for

the

for responsibility

had

had plant

The

department

sales schedules.

The ery

plant

responsibility

Incentives

Man~~~1!_t

sole

with

manager

in line

profits:

Plant managers were motivated to meet their profit goals in a number of ways. First, only capable managers were promoted, with profit performance being a main factor in determining capability. Second, plant managers' compensation packages were tied to achieving profit budgets. Third, each month a

chart was compiled showing manufacturing efficienct by plant and division. These comparative efficiency charts were highly publicized by most plant managers despite the inherent unfairness in comparing plants that produced different products requiring different setup times, etc. Some plants ran internal competitions between production lines and departments to reduce certain cost items, rewarding department heads and foremen for their accomplishments.

Questions 1. Outline the strengths and weaknesses ofVershire Company's planning and control

system.

2. Trace the profit budgeting process at Vershire, starting in May and ending

with the Board of.Directors' meeting in December.Be prepared to describe the activities that took place at each step of the processand present the rationale for each. 3. Should the plant managersbe held responsiblefor profits? Why?Why not? 4. How do you assessthe performanceevaluation systemcontainedin Exhibits 2 and

3?

5. On balance,would you redesign the managementcontrol structure at Vershire

Company?

If so, how

and why?

Vershire Company

'Numbers

in this exhibit

6

have been'omitted,

--

~,'

.

several

shows

divi-

the

to

1

man-

with largest

the Exhibit Reporting

States.

of

company

packaging division-one

United

division.

the

in

Can

Aluminum

cans

Can

diversified

a

was

Aluminum the

for

beverage

the

Company chart

aluminum

including

Vershire

of

divisions, organization

the

ufacturers

major

1996

Company

In

Vershire

sional general manager were two line managers, vice presidents in charge of manufacturing and marketing. These vice presidents headed all of the division's activities in their respective functional areas.

The Aluminum Can division's growth in salesslightly outpacedsalesgrowth in the industry at large. The division had plants scattered throughout the United States. Each plant served customers in its own geographic region, often producing several different sizes of cans for a range of customers that included

both large and small breweries and soft drink bottlers. Most of these customers had between two and four suppliers and spread purchases among them. If the division failed to meet the customer's cost and quality speciijcations or its stan-

dards for delivery and customer service,the customer would turn to another supplier. All aluminum can producers employed essentially the same technology, and the division's product quality was equal to that of its competitors.

con-

aluminum,

metal

The

materials: plastic.

or

several

of

one composite),

from

made

metal

and

were (paper

fiber-foil

glass,

steel,

containers

Backgroundl

Traditionally,

Industry

tainer industry consisted of the hundred-plus firms that produced aluminum

EXHIBIT 1

AluminumCan

Vijay

Professors

of

supervision

the

(T'94)

Chitkar~

This case was adapted by Anil R.

under

Division

Hawkins.

David

Professor

by

pared

Govindarajanand RobertN. Anthony.The caseis based(with permission)on ~n earliercasepre-

Harvarn

Hamerm~h

Professor

by

prepared

case,

1Theindustry backgroundis basedon a similardescriptionin the Crown Cork and SealCompany R".inA" -:rh~1

2

Company

and tin-plated steel cans. Aluminum cans were used for packaging beverages (beer and soft drinks), while tin-plated steel cans were used primarily for food packaging, paints, and aerosols. In 1970, steel cans ed for 88 percent of metal

pri-

of were

percent

75 containers

over

the

for

had come to dominate

purchased

ed who

cans bottlers

aluminum

but by the 1990s aluminum

drink

soft

1996,

In production.

The

industry.

the can

the metal can production,

cost

64

it for

and

lines

five

ed

was typically

plant

container

materials

a Raw

for line.

scale per

efficient equipment

in

minimum

The

million

$20

ket.

marily small independent franchisees of Coca-Cola and Pepsi Cola, which represented their independent bottlers in negotiating with the container companies. Five beverage container manufacturers ed for 88 percent of the mar-

percent of the production cost. Other costs included labor (15 percent), marketing and general istration (9 percent), transportation (8 percent), depreciation (2 percent), and research and development (2 percent). For beverage processors, the cost of the can usually exceeded the cost of the contents, with the container ing for approximately 40 percent of the to-

tal manufacturing cost.Most beverageprocessorsmaintained two or more suppliers;

and

some

processors

integrated

backward,

manufacturing

cans

themselves.On~ large beveragecompany produced one-third of its own container requirements and ranked ducers in the industry.

as one of the top five beverage container

pro-

efficient,

a more

and

cup even

deep

a become

into had

pushed process

was

metal

of manufacturing

sheet the

flat

a

producing

1996

By

which

in attached.

process was

top

piece

Prior to the early 1970s, cans were produced by rolling a sheet of steel, soldering and cutting it to size, and attaching both the top and the bottom. In 1972 the industry was revolutionized when aluminum producers perfected a two-

over 2,000 cans per minute.

In addition to production efficiency,aluminum had other advantagesover

a

was

reduced

it

and

it pernlitted

aluminum

lithograph;

to

of flavoring;

Additionally;

easier

was

weight.

it lighter

its

because

of

because

packaging costs

attractive

more

steel: It was easier to shape; it reduced the problems

transportation

Vershire

more attractive recycling material, with a ton of scrap aluminum having almost three times the value of a ton of scrap steel. Four global companies supplied alu-

minum to can producers:Alcoa,Alcan, Reynolds,and Kaiser.Two of thesecompanies, Alcoa and Reynolds, also manufactured

Divisions

of Vershire

Company

were structured

aluminum

containers.

to encom

broad product

categories. Divisional general managers were given full control of their busi-

nesseswith two exceptions:the raising of capital and labor relations,which were both centralized at head office. The budget was used as the primary to direct each division's efforts towards common corporate objectives.

tool

In May,eachdivisionalgeneralmanagersubmitteda preliminaryreport to corporate

management

summarizing

the outlook

for sales,

income.

and caDital

3

Company

re-

detailed

not

already

were

was

reports

division

These

each

since

years.

two together

pull

to

subsequent

the

easy

over

fairly

category

usually

each

were

and

in

requirements for the next budget year, and evaluating the trends anticipated

quired to predict market conditions in the current year and to anticipate capital expenditures five years out as part of the strategic planning process. Once the divisional

general

managers

had submitted

these preliminary

re-

to

fore-

budget sales combined

A

forthcoming

were

.

the general

forecasts

these

more

exaInining in and

years division;

each

two

assessment,

market

following

for

the

formal prepared

and

more

a

detail

then

in was

year

velop

ports, the central market researchstaff at corporateheadquartersbeganto de-

cast

Vershire

create a forecast for the entire company. In developing division forecasts, the research staff considered several topics, including general econoInic conditions and their impact on customers, and market share for different products by geographic area. Fundamental assumptions were made as to price, new products, changes in particular s, new

plants, inventory carryovers, forward buying, packaging trends, industry growth trends, weather conditions, and alternative packaging.Each product line, regardlessof size,was reviewed in the samemanner. These foreca~ts were prepared at the head office in order to ensure that basic assumptions were uniform and that overall corporate sales forecasts were

both reasonable and achievable.The completed forecasts were forwarded to their

respective

divisions

for review,

criticism,

and fine-tuning.

The divisional general managers then compiled their own sales forecasts from

the bottom

up, asking

each district

sales manager

to estimate

sales for the

comingbudget year.The district managerscould requesthelp from the head office or the divisional staff but in the end assumed full responsibility for the forecasts they submitted. All district sales forecasts were consolidated at the division level for review by the vice president for marketing, but no changes were made in a district's forecast unless the district manager agreed. Likewise, once the budget had been approved, any changes had to be approved by all those responsible for that budget.

This processwas then repeated at the corporatelevel. When all the responsible parties were satisfied with the sales budget, the figures became fIXed ob-

jectives,with eachdistrict being held responsiblefor its own portion. The entire review

and approval

process

had

four

objectives:

1. To assesseachdivision's competitiveposition and formulate coursesof action to improve

upon

it.

2. To evaluate actions taken to increase market share or to respond to competitors'

activities.

3. To considerundertaking capital expendituresor plant alterations to improve existing

products

or introduce

new products.

4. To developplans to improve cost efficiency,product quality, delivery methods, and service.

~~facturing~~~~~ Mer

final approval at the divisional and corporate levels, the overall sales

budget was translated into a salesbudget for each plant, broken down accord-

4

end use. Onc~ the sales numbers

were estimated,

budgeted

plant

and

the

At volume,

shipped.

each plant

price,

be

to

would according

goods

finished

categorized

the then

which

was

from budget

plants sales

the

to

the

level,

ing

Company

gross profit,

fIXed expenses,and pretax income. Profit was calculated as the sales budget less budgetedvariable costs(including direct material, direct labor, and variable manufacturing overhead-each valued at a standard rate) and the fixed overhead budget. The plant manager was held responsiblefor this budgeted profit number even if actual sales fell below the projected level. Cost standards and cost reduction targets were developed by the plant's industrial engineering department, which also determined budget performance standards for each department, operation, and cost center within the plantincluding such items as budgeted cost reductions, allowances for unfavorable

variancesfrom standards,and fixed costssuch as maintenancelabor. Before plant budgets were submitted, controller staff from the head office visited each plant. These visits were extremely important because they provided an opportunity for plant managers to explain their situation and allowed controllers to familiarize themselves with the reasoning behind the managers' numbers so that they could better explain them when they were presented to corporate management. The controllers also used these visits to provide guidance as to whether the budgeted profits were in line with corporate goals, and

to reinforce the' notion that headquarters was in touch with the plant. Each visit usually lasted about half a day. Most of the time was devotedto

ployees

were

plant

em-

a the

for what)

allocated

(and

also how

was

time

but

themselves

for

see

meetings;

the

could

in

include

controllers

to

so

wished walk-through

agers

reviewing the budget with the plant manager and any supervisors the man-

doing.

On or beforeSeptember1,plant budgetswere submitted to the division head

When

for

was

ap-

asked

for

or

budget

savings. submitted

it

the

additional

budget,

was

approved

the

for

look

either December.

in

budget

who

with

to

asked

satisfied (CEO), consolidated meeting

final

Officer

was

were

managers

Directors

of

Board

The

Executive

manager

plant

general Chief the

at

modifications.

the

divisional

to certain

sent

the

expectations,

office, where they were consolidated and presented to the divisional general managers for review. If the budgets were not quite in line with management's

proval

Vershire

Oncea budget had been approved,it was difficult to change.Any problems that arose between sales and production at a given plant were expected to be solved by people in the field. If a customer called with a rush order that would disrupt production, for example, production could recommend various courses of

action but it was the salesmanager'sresponsibility to get the product to the customer. If the sales manager determined that it was essential to ship the product

right away,that would be done.The customerwas alwaysthe primary concern. Performance

--

Measurement

and

Evaluation

On the secondbusinessday after the closeof eachmonth, every plant faxed certain critical operating varianceswhich were combinedinto a "variance analysis sheet."A compilation of all variance sheetswas distributed the following morning to interested management. Plant managers were not supposed to wait until these monthly statements were prepared to identify unfavorable variances;

Vershire Comoanv

5

rather, they were expectedto be aware of them (and to take correctiveaction)on a daily

basis.

which budgetedtargets had not beenmet.The focuswason net sales,in-

in

areas

Four business days after the close of every month, each plant submitted a report showing budgeted and actual results. Onee these reports were received, corporate management reviewed the variances for those items where figures exceededbudgetary amounts, thus requiring plant managers to explain only the cluding price and mix changes, gross margin, and standard manufacturingcosts. The budgeted and actual information submitted is summarized in Exhibit 2. Supplemental information was provided by ing documents (see Exhibit

3). Both reports were consolidatedfor eachdivision and for the entire company, and distributed

the next day.

The fIXedcostswere examinedto seeif the plants had carried out their various programs,if the programs had met budgetedcosts,and if the results were expectations.

deliv-

and

and

mix, operations

sales plant

price,

for

the

for responsibility

had

had plant

The

department

sales schedules.

The ery

plant

responsibility

Incentives

Man~~~1!_t

sole

with

manager

in line

profits:

Plant managers were motivated to meet their profit goals in a number of ways. First, only capable managers were promoted, with profit performance being a main factor in determining capability. Second, plant managers' compensation packages were tied to achieving profit budgets. Third, each month a

chart was compiled showing manufacturing efficienct by plant and division. These comparative efficiency charts were highly publicized by most plant managers despite the inherent unfairness in comparing plants that produced different products requiring different setup times, etc. Some plants ran internal competitions between production lines and departments to reduce certain cost items, rewarding department heads and foremen for their accomplishments.

Questions 1. Outline the strengths and weaknesses ofVershire Company's planning and control

system.

2. Trace the profit budgeting process at Vershire, starting in May and ending

with the Board of.Directors' meeting in December.Be prepared to describe the activities that took place at each step of the processand present the rationale for each. 3. Should the plant managersbe held responsiblefor profits? Why?Why not? 4. How do you assessthe performanceevaluation systemcontainedin Exhibits 2 and

3?

5. On balance,would you redesign the managementcontrol structure at Vershire

Company?

If so, how

and why?

Vershire Company

'Numbers

in this exhibit

6

have been'omitted,

--

~,'

.

Related Documents c2h70

Case Solution - Vershire Company 4i1h2l

December 2019 31

Vershire Company Case Print 30141s

April 2021 0

Case Study - Vershire Company 59205l

April 2021 0

Dashman Company Case Solution. 4k172j

January 2022 0

Solution Case Birch Paper Company 4f2r5x

December 2021 0

Baldwin Bicycle Company Case Solution Excel File 40231m

November 2019 103More Documents from "Jerelleen Rodriguez" 3g1570

Case Solution - Vershire Company 4i1h2l

December 2019 31

Quality Metal Service Center - Final 5u5d57

December 2021 0

6g3p1u

December 2019 88

6g3p1u

December 2019 135

6g3p1u

May 2021 0