2016 Level I Errata 38b4n

This document was ed by and they confirmed that they have the permission to share it. If you are author or own the copyright of this book, please report to us by using this report form. Report 2z6p3t

Overview 5o1f4z

& View 2016 Level I Errata as PDF for free.

More details 6z3438

- Words: 1,064

- Pages: 3

2016 CFA Program: Level I Errata 24 October 2016

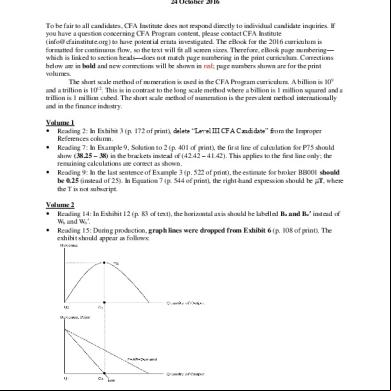

To be fair to all candidates, CFA Institute does not respond directly to individual candidate inquiries. If you have a question concerning CFA Program content, please CFA Institute ([email protected]) to have potential errata investigated. The eBook for the 2016 curriculum is formatted for continuous flow, so the text will fit all screen sizes. Therefore, eBook page numbering— which is linked to section heads—does not match page numbering in the print curriculum. Corrections below are in bold and new corrections will be shown in red; page numbers shown are for the print volumes. The short scale method of numeration is used in the CFA Program curriculum. A billion is 109 and a trillion is 1012. This is in contrast to the long scale method where a billion is 1 million squared and a trillion is 1 million cubed. The short scale method of numeration is the prevalent method internationally and in the finance industry. Volume 1 Reading 2: In Exhibit 3 (p. 172 of print), delete “Level III CFA Candidate” from the Improper References column. Reading 7: In Example 9, Solution to 2 (p. 401 of print), the first line of calculation for P75 should show (38.25 – 38) in the brackets instead of (42.42 – 41.42). This applies to the first line only; the remaining calculations are correct as shown. Reading 9: In the last sentence of Example 3 (p. 522 of print), the estimate for broker BB001 should be 0.25 (instead of 25). In Equation 7 (p. 544 of print), the right-hand expression should be T, where the T is not subscript. Volume 2 Reading 14: In Exhibit 12 (p. 83 of text), the horizontal axis should be labelled Ba and Baʹ instead of Wb and Wbʹ. Reading 15: During production, graph lines were dropped from Exhibit 6 (p. 108 of print). The exhibit should appear as follows:

Reading 17: In Example 4 (p. 230 of print), change the federalprovincial government deficit to 84,249 (instead of 82,249) in the question and in the next-to-last paragraph of the solution. This changes the domestic private saving to 69.5 percent (instead of 71 percent) and the excess imports to C$25,661 (instead of 23,661). Reading 18: During production, an error was introduced in format. Seven (7) instances of M2 should be changed to M2 (no superscript).

Volume 3 Reading 23: In Exhibit 8 (p. 64 of print), the bolded sub-total of 150,000 should appear under Contributed Capital instead of Retained Earnings. Reading 27: In Exhibit 12 (p. 296 of print), Groupe Danone’s line item “Other flows with no impact on cash” should be 98 for 2008 and (72) for 2009.

Reading 28: In the Solution to Example 17 (p. 379 of print), the formula for Segment ROA should show division vs. multiplication in the term bolded: “Segment ROA = Segment operating income/Segment assets = (Segment operating income/Segment revenue) × (Segment revenue/Segment Assets) = Segment margin × Segment turnover.” Reading 29: In Example 5, in the last line of Solution to 7 (p. 410 of print), inventory would increase by $3,183 million under FIFO (instead of $3,153 million). Reading 30: In Exhibit 5 (p. 466 of print), Net Income for 2008 should total $7,994 and EPS is $0.82 (instead of $7,934 and $0.81 respectively). The solution to Practice Problem 14 (p. 528 of print) should show “Impairment = max(Recoverable amount Fair value less costs to sell; Value in use) – Net carrying amount”. The numerical solution is unchanged. Reading 33: In Example 7 (p. 653 of print), the sentence immediately below the table should begin as follows: “During the period, the company sells, at $250 each, all of the goods purchased ….” Reading 34: Candidates should delete Practice Problem 8 (p. 728) and its solution (p. 730). This question is no longer assigned.

Volume 4 Reading 43: In the solution to Practice Problem 7 (p. 385 of print), the equation should solve to 12.11% instead of 2.11. In the solution to Practice Problem 35 (p. 388 of print), change “minimumvariance frontier” to “efficient frontier” in two places. Volume 5 Reading 47: In Equation 4 (p. 80 of print), delete the =1 from the end of the formula. Reading 49: The formula in Solution 12 (p. 184 of print) should show Pt-1 as the denominator, instead of Pt. The solution was correctly calculated; only the subscript is changed. Reading 50: In the first column of Exhibit 7 (p. 219 of print), the second line item should be “Barriers to Entry” instead of Barriers to Entry/Success. Reading 53: There are a number of edits in this reading: o In Exhibit 8 (p. 374 of print), Eurocommercial Paper may be on an interest-bearing or discount basis. o In the paragraph below Exhibit 8, make the following edits: “In contrast, E is usually may be issued at, and trade on, an interest-bearing or yield basis or a discount basis. In other words, the rate quoted on a trade of E is the actual interest rate earned on the investment, and the interest payment is made in addition to the par value at maturity.” o In the solution to Practice Problem 17 (p. 396 of print), “C is incorrect because Eurocommerical paper may be issued on an interest-bearing (or yield) basis or a discount basis.” Reading 54: In Equation 14 (p. 434 of print), the final expression should appear as (1 + zB)B.

Reading 56: In the solution to Practice Problem #6 (top of p. 577 of print), reinvested cash flows are at 8% instead of 6%.

Volume 6 Reading 58: In the second paragraph above Section 4.2.2 beginning “Before leaving options …” (p. 30 of print), change the second sentence to read: “With the former forward commitments, the parties agree to trade an underlying asset at a later date …” Reading 59: In Example 4, question 2 (p. 81 of print), change option A to “Interest rates are known constant.” Change Solution to 2 (p. 82) to read: “C is correct. Known Constant interest rates and or the condition that futures prices are uncorrelated with forward prices interest rates will make forward and futures prices equivalent. The volatility of forward and futures prices has no relationship to any difference.”

To be fair to all candidates, CFA Institute does not respond directly to individual candidate inquiries. If you have a question concerning CFA Program content, please CFA Institute ([email protected]) to have potential errata investigated. The eBook for the 2016 curriculum is formatted for continuous flow, so the text will fit all screen sizes. Therefore, eBook page numbering— which is linked to section heads—does not match page numbering in the print curriculum. Corrections below are in bold and new corrections will be shown in red; page numbers shown are for the print volumes. The short scale method of numeration is used in the CFA Program curriculum. A billion is 109 and a trillion is 1012. This is in contrast to the long scale method where a billion is 1 million squared and a trillion is 1 million cubed. The short scale method of numeration is the prevalent method internationally and in the finance industry. Volume 1 Reading 2: In Exhibit 3 (p. 172 of print), delete “Level III CFA Candidate” from the Improper References column. Reading 7: In Example 9, Solution to 2 (p. 401 of print), the first line of calculation for P75 should show (38.25 – 38) in the brackets instead of (42.42 – 41.42). This applies to the first line only; the remaining calculations are correct as shown. Reading 9: In the last sentence of Example 3 (p. 522 of print), the estimate for broker BB001 should be 0.25 (instead of 25). In Equation 7 (p. 544 of print), the right-hand expression should be T, where the T is not subscript. Volume 2 Reading 14: In Exhibit 12 (p. 83 of text), the horizontal axis should be labelled Ba and Baʹ instead of Wb and Wbʹ. Reading 15: During production, graph lines were dropped from Exhibit 6 (p. 108 of print). The exhibit should appear as follows:

Reading 17: In Example 4 (p. 230 of print), change the federalprovincial government deficit to 84,249 (instead of 82,249) in the question and in the next-to-last paragraph of the solution. This changes the domestic private saving to 69.5 percent (instead of 71 percent) and the excess imports to C$25,661 (instead of 23,661). Reading 18: During production, an error was introduced in format. Seven (7) instances of M2 should be changed to M2 (no superscript).

Volume 3 Reading 23: In Exhibit 8 (p. 64 of print), the bolded sub-total of 150,000 should appear under Contributed Capital instead of Retained Earnings. Reading 27: In Exhibit 12 (p. 296 of print), Groupe Danone’s line item “Other flows with no impact on cash” should be 98 for 2008 and (72) for 2009.

Reading 28: In the Solution to Example 17 (p. 379 of print), the formula for Segment ROA should show division vs. multiplication in the term bolded: “Segment ROA = Segment operating income/Segment assets = (Segment operating income/Segment revenue) × (Segment revenue/Segment Assets) = Segment margin × Segment turnover.” Reading 29: In Example 5, in the last line of Solution to 7 (p. 410 of print), inventory would increase by $3,183 million under FIFO (instead of $3,153 million). Reading 30: In Exhibit 5 (p. 466 of print), Net Income for 2008 should total $7,994 and EPS is $0.82 (instead of $7,934 and $0.81 respectively). The solution to Practice Problem 14 (p. 528 of print) should show “Impairment = max(Recoverable amount Fair value less costs to sell; Value in use) – Net carrying amount”. The numerical solution is unchanged. Reading 33: In Example 7 (p. 653 of print), the sentence immediately below the table should begin as follows: “During the period, the company sells, at $250 each, all of the goods purchased ….” Reading 34: Candidates should delete Practice Problem 8 (p. 728) and its solution (p. 730). This question is no longer assigned.

Volume 4 Reading 43: In the solution to Practice Problem 7 (p. 385 of print), the equation should solve to 12.11% instead of 2.11. In the solution to Practice Problem 35 (p. 388 of print), change “minimumvariance frontier” to “efficient frontier” in two places. Volume 5 Reading 47: In Equation 4 (p. 80 of print), delete the =1 from the end of the formula. Reading 49: The formula in Solution 12 (p. 184 of print) should show Pt-1 as the denominator, instead of Pt. The solution was correctly calculated; only the subscript is changed. Reading 50: In the first column of Exhibit 7 (p. 219 of print), the second line item should be “Barriers to Entry” instead of Barriers to Entry/Success. Reading 53: There are a number of edits in this reading: o In Exhibit 8 (p. 374 of print), Eurocommercial Paper may be on an interest-bearing or discount basis. o In the paragraph below Exhibit 8, make the following edits: “In contrast, E is usually may be issued at, and trade on, an interest-bearing or yield basis or a discount basis. In other words, the rate quoted on a trade of E is the actual interest rate earned on the investment, and the interest payment is made in addition to the par value at maturity.” o In the solution to Practice Problem 17 (p. 396 of print), “C is incorrect because Eurocommerical paper may be issued on an interest-bearing (or yield) basis or a discount basis.” Reading 54: In Equation 14 (p. 434 of print), the final expression should appear as (1 + zB)B.

Reading 56: In the solution to Practice Problem #6 (top of p. 577 of print), reinvested cash flows are at 8% instead of 6%.

Volume 6 Reading 58: In the second paragraph above Section 4.2.2 beginning “Before leaving options …” (p. 30 of print), change the second sentence to read: “With the former forward commitments, the parties agree to trade an underlying asset at a later date …” Reading 59: In Example 4, question 2 (p. 81 of print), change option A to “Interest rates are known constant.” Change Solution to 2 (p. 82) to read: “C is correct. Known Constant interest rates and or the condition that futures prices are uncorrelated with forward prices interest rates will make forward and futures prices equivalent. The volatility of forward and futures prices has no relationship to any difference.”

Related Documents c2h70

2016 Level I Errata 38b4n

October 2019 55

Cfa 2016 Level I Errata 5u6h50

August 2021 0

2017 Level I Errata 5zt19

December 2019 34

2016 Cfa Level Iii Errata 185x1l

November 2019 53

Nbr-7181-2016 Errata p22u

October 2020 0

Nbr 5738 - 2016 Errata 723m6n

October 2019 81More Documents from "Musafir" 3b6t48

The Art Of War Bangla.pdf 585n2j

November 2021 0

The Art Of War Bangla.pdf 585n2j

November 2021 0

6g3p1u

December 2019 119

Abol-tabol-sukumar-roy.pdf 3t1v2l

December 2019 50

2016 Level I Errata 38b4n

October 2019 55